The Cost of Waiting to Buy a Home: Interest Rates vs. Rising Property Values |Hideaway Properties | Blog

In the world of real estate, timing is everything. Lately, many potential homebuyers are hesitating to make a purchase, hoping for interest rates to drop. However, waiting for a more favorable interest rate could end up costing more in the long run. Let’s delve into why this is the case. See the example below, provided by a trusted lending advisor, of waiting to buy our current listing in Dillon Beach for a real life example.

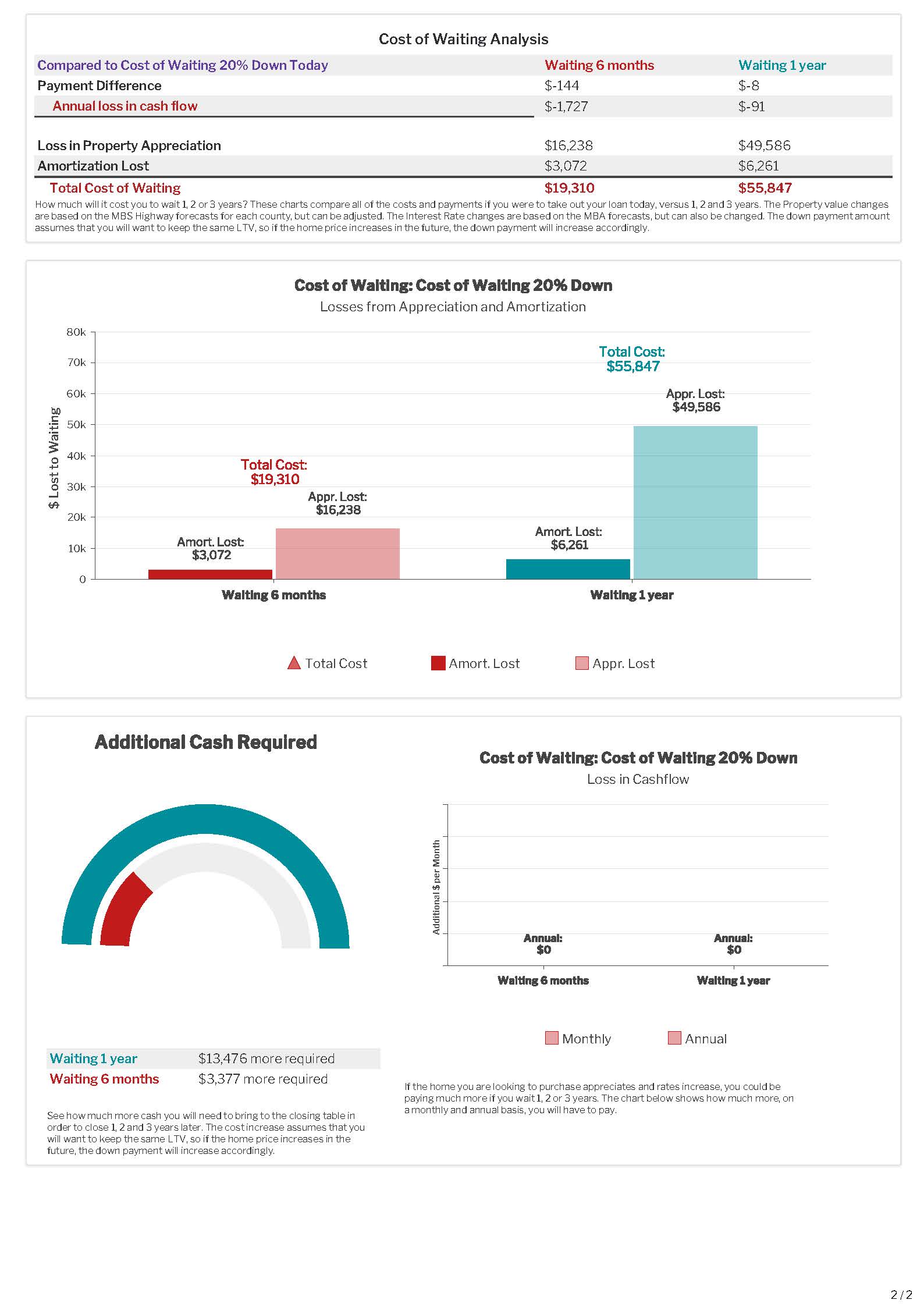

The Ascent of Property Values

One of the most significant factors to consider is the consistent rise in property values. Even as you wait for interest rates to fall, the price of real estate continues to climb. Waiting six months to a year could mean facing even higher home prices down the line. This increase leads to a higher down payment and a larger total loan amount, which may offset any savings from a potential decrease in interest rates.

For example, if a $849,000 home appreciates by 5.84% over the next year as anticipated, that’s an additional $50,000 you would have to pay for the same house. Even if interest rates drop, you could still end up paying more overall because of the increased loan amount and down payment.

Lost Appreciation

When you delay purchasing a home, you also miss out on the property appreciation that current homeowners are enjoying. Home equity builds as property values rise, contributing to your overall net worth and financial stability. By waiting to buy, you’re losing out on this essential wealth-building opportunity, making it harder for you to invest and grow your money in other ways.

Forgone Loan Amortization

Each mortgage payment you make contributes to the amortization of your loan, gradually reducing your debt and increasing your equity in the property. If you postpone buying a home, you miss out on this valuable loan amortization. In the meantime, you’re likely paying rent, which doesn’t contribute to building equity or wealth, further exacerbating the cost of waiting.

Increased Competition

When mortgage rates drop, it invariably attracts a surge in prospective homebuyers, intensifying the competition to buy a home. Lower interest rates make home buying more affordable, widening the pool of eligible buyers. This increased demand often leads to bidding wars, driving up the prices of available properties. As more people rush to take advantage of the favorable rates, the inventory of available homes shrinks, exacerbating the competition further. Even as buyers save on interest, the heightened demand and elevated prices could negate those savings. Prospective buyers should carefully weigh these factors, understanding that waiting for lower mortgage rates does not necessarily guarantee overall cost savings in a competitive market.

Conclusion

In conclusion, while it’s essential to consider interest rates when purchasing a home, it’s equally crucial to think about rising property values, lost appreciation, forgone loan amortization, and increased competition of buyers. You can also refinance your home later when interest rates drop. Remember that real estate typically appreciates over time, making it a solid investment even when interest rates are higher. If you’re financially prepared to buy a home, it may be wise to make the move now rather than waiting for an uncertain future drop in interest rates, which may be offset by rising property values. Consult with a financial advisor and a real estate professional to understand all the factors at play and make an informed decision. See the below real life example for 12 Ocean View Avenue in Dillon Beach.

Stay up to date on the latest real estate trends.

March 17, 2025

Our professional expertise and ethical partnership are the best ways to protect you from the potential pitfalls of going it alone.

January 23, 2024

A guide to the life expectancy of systems and features of a typical home

November 28, 2023

Homeseller concessions return

September 30, 2023

Marry the Home - Date the Rate

April 19, 2023

January 4, 2023

(And what it means for you)

You’ve got questions and we can’t wait to answer them.